Location Based Services Market: By Components (Solutions, Services); Location Type (Indoor, Outdoor); Technology (Global Positioning System (GPS), Global Navigation Satellite System (GNSS), Wi-Fi, Cellular ID, Bluetooth Beacons, Others); Application (Inventory Monitoring, Mapping & GIS, Asset Tracking, Proximity Marketing, Social Networking, Fleet Management, Navigation, Business Intelligence & Analytics); End User ( BFSI, Manufacturing, Retail, Healthcare & Life Science, IT & Telecom, Hospitality, Transportation & Logistics, Government, Media & Entertainment, Aerospace & Défense, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 05-Dec-2025 | | Report ID: AA0223364

Markey Snapshot

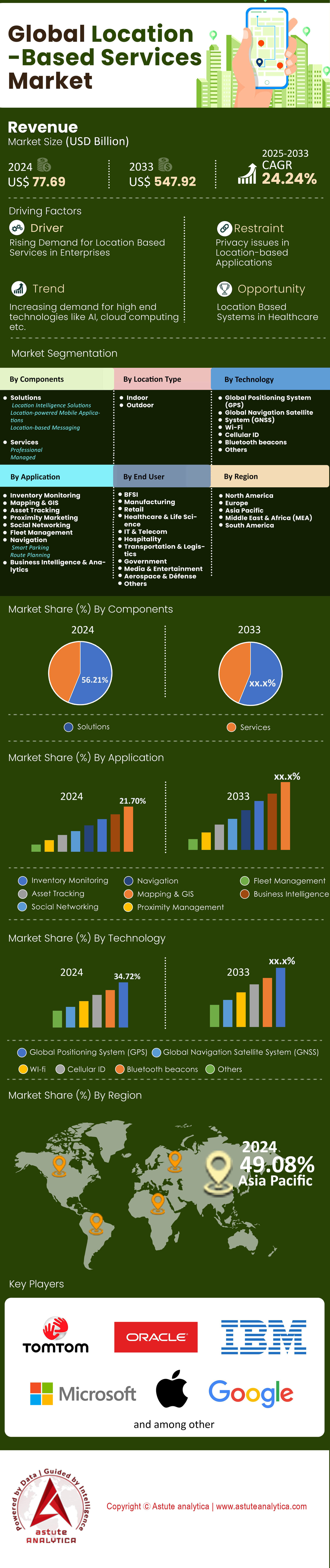

Location based services market generated a revenue of US$ 77.69 billion in 2024 and it is estimated to reach a valuation of US$ 547.92 billion by 2033 at a CAGR of 24.24% during the forecast period from 2025–2033.

Key Findings

- Based on location, outdoor location services has captured a 63.1% share of the market.

- Based on technology, GPS (Global Positioning System) dominates the technology landscape of market with 34.72% market share.

- Based on application, Mapping and Geographic Information System (GIS) section has taken up a big share of 21.5%.

- Based on end-users, transport and logistics segment is the global location-based services market with over 17.6% stake.

- Asia Pacific alone accounts for over 50% market share.

The fundamental driver of location-based services market growth has shifted from simple navigation to operational certainty. In previous years, a 5-meter variance in GPS was acceptable for a ride-share pickup; today, autonomous systems and drone logistics require sub-decimeter precision. The market is expanding because technology finally meets these commercial demands. Standard GPS Signal-in-Space Error (SISRE) has improved to 30 cm (RMS), but the real catalyst is the commercialization of PPP-RTK systems, which now offer 3.3 cm 3D-RMS accuracy.

The leap in fidelity allows location-based services market to penetrate industries that previously could not rely on it. For instance, the reduction of convergence time (the time to lock into high precision) to just 5.4 minutes removes the operational bottleneck for drone delivery and robotic agriculture. Furthermore, the standardization of update rates at 10 Hz to 20 Hz for commercial hardware means that fast-moving assets can now be tracked safely. The growth is being underwritten by the efficiency gains these specs provide: reducing the Cold Start time to 2–10 seconds via network assistance fundamentally changes the user experience in urban logistics, driving adoption in sectors where time is literally money.

To Get more Insights, Request A Free Sample

Who Are the Primary Consumers Driving Demand Beyond Smartphones?

While the 4.88 billion global smartphone users remain the base layer of the location-based services market pyramid, the high-value consumption is pivoting rapidly toward B2B enterprises in logistics, retail, and healthcare. These consumers are not buying "maps"; they are buying efficiency and risk reduction. The logistics sector is a primary consumer, driven by the need to mitigate the USD 3.1 Trillion annual loss US businesses face due to bad location data. Specifically, companies are investing heavily to eliminate the USD 20 billion annual cost of undeliverable mail.

Healthcare and construction have also emerged as aggressive consumers of indoor positioning in the location-based services market. With nurses spending 1 hour per shift searching for assets, hospitals are adopting Real-Time Location Systems (RTLS) to cut this to under 10 minutes. Similarly, construction firms facing 14 hours of downtime per person annually are deploying tracking to reduce wasted time by 40%. In the retail space, advertisers are major consumers of location intelligence, paying a Cost Per Visit (CPV) of USD 0.20 to USD 0.60 to drive foot traffic. The "consumer" profile has thus evolved from a driver looking for a coffee shop to an algorithm optimizing a supply chain or a marketing budget.

How Are Major Players Like Google and Mobileye Redefining Competition?

The competitive landscape of the location-based services market is defined by a battle between "Generalist Map Providers" and "Specialized Autonomy Platforms." Google and Mapbox are fighting a price war for the developer ecosystem. With Google Maps Platform charging USD 7.00 per 1,000 dynamic loads, Mapbox has positioned itself as the cost-efficient alternative at USD 5.00 per 1,000 loads. This 28% price undercut is forcing a commoditization of standard web mapping, pushing competitors to differentiate via data richness rather than just coverage.

On the autonomy front, Mobileye is leveraging a massive data moat in the location-based services market. By collecting 47.6 billion kilometers of driving data in just one year (2024), bringing their total to 91.1 billion kilometers, they have created a "living map" that is self-healing. This contrasts with legacy players relying on survey fleets. TomTom, with its Orbis map covering 86 million kilometers, is aggressively targeting the collaborative mapping space to counter this. Meanwhile, the sheer volume of intellectual property indicates a fierce battle for technical supremacy; major players like Waymo, Bosch, and Huawei hold the majority of the 5,433 active patents in visual positioning. They are staying competitive not just by mapping roads, but by owning the sensor fusion IP that interprets them.

Where Are the Most Lucrative Growth Opportunities Geographically?

Geographically, the opportunity across the location-based services market is split between "Infrastructure Density" in the West and "Scale" in the East. The United States and Europe remain the lucrative hubs for high-ARPU verticals like Ad-Tech and Insurance Telematics, where Usage-Based Insurance (UBI) is growing at a 16% CAGR. The willingness to pay for privacy-compliant, high-fidelity data is highest here, supported by ad CPMs reaching USD 32.75 for location-targeted video.

However, the hardware and infrastructure growth is heavily tilted toward regions deploying 5G aggressively in the location-based services market. The small cell market, critical for LBS accuracy, is growing at a 21.5% CAGR to reach USD 11.4 billion, with massive deployments in dense urban centers of Asia and North America. Notably, China and the US together account for over 50% of global filings in autonomous perception patents, signaling that these two markets will dictate the standards for the next decade. The deployment of 5G networks capable of supporting 1 million connected devices per square kilometer in these regions creates the fertile ground necessary for massive IoT tracking.

What Technological Disruptions Are Reshaping the Landscape?

Two major disruptions are fundamentally altering the location-based services market: Sensor Fusion and Indoor Precision. The reliance on GPS alone is ending. The industry is pivoting toward "Sensor Fusion," where cameras, radar, and Lidar corroborate location. This is evidenced by the explosive 1,100% growth in 4D imaging radar patents. This technology allows vehicles to "see" their location relative to landmarks, rather than just receiving coordinates from space.

Simultaneously, the "Indoor Blind Spot" is being illuminated by Ultra-Wideband (UWB). With accuracy of 10–30 cm, UWB is disrupting the legacy Bluetooth beacon market (1–3 meter accuracy). This shift is critical because it enables interaction, not just tracking. However, this comes with a cost: 5G positioning consumes 10–20% more power than 4G, and continuous tracking drains 13% of a battery per hour. This creates a market gap for low-power innovations, such as Angle of Arrival (AoA) BLE 5.1, which promises sub-meter accuracy without the battery penalty.

How Are Privacy Trends and Ad Fraud Influencing Market Stability?

The most volatile variable in the location-based services market outlook is user behavior regarding privacy. The "Always On" tracking era is over. With iOS ATT opt-in rates hovering at just 13.85%, and only 15–20% of users retaining background permissions after 30 days, the volume of third-party location data is shrinking. This scarcity is driving up the price of high-quality, consented data. "Fresh" data is now a premium asset, especially considering B2B data decays at 22.5% to 70.3% annually.

This scarcity also invites fraud in the location-based services market. With global location ad fraud averaging 14% and hitting 60% in competitive sectors, the market is seeing a surge in demand for verification tools. Platforms that can prove the veracity of a visit—filtering out the bots and spoofed GPS signals—will capture the premium ad budgets. Consequently, the market is bifurcating: low-quality, non-compliant data is becoming worthless, while first-party, high-fidelity data segments are seeing their value skyrocket to USD 5.00+ CPM. Future growth belongs to platforms that can navigate this privacy-efficiency paradox.

Segmental Analysis

Why Does the Great Outdoors Still Command the Market? (63.1% Share)

It might seem counterintuitive that in an increasingly indoor-centric digital world, the Outdoor Location Services segment still commands a massive 63.1% of the global location-based services market in 2025. The reason isn't just about people looking for directions; it’s about a fundamental shift in accuracy. We have moved past the era of standard 5-meter GPS bubbles. The market is now driven by the commercial explosion of Precision Point Positioning (PPP) and Real-Time Kinematic (RTK) services delivered directly over 5G networks. This "lane-level" precision—often sub-decimeter—is the invisible infrastructure keeping the chaotic micro-mobility sector alive. LBS providers are essentially selling safety and compliance; they monetize the specific correction data that tells an e-scooter operator whether a rider is safely in a bike lane or illegally on a sidewalk, or allows an insurance adjuster to reconstruct an accident scene with forensic accuracy using trajectory data rather than guesswork.

The dominance of this segment in the location-based services market is further cemented by the fact that "outdoor" connectivity no longer has dead zones. Thanks to the full deployment of 3GPP Release 17 and 18 standards, devices now utilize Non-Terrestrial Networks (NTN). This means your tracking hardware seamlessly hands off the signal from a terrestrial 5G tower to a Low Earth Orbit (LEO) satellite without the user ever noticing a drop. This capability has opened up entirely new revenue channels in remote industrial management. Oil, gas, and utility companies are paying premiums for "hybrid positioning" software layers that fuse GNSS, cellular, and Wi-Fi data into a single, unbreakable lock. By solving the connectivity gap in remote regions, outdoor services have become indispensable for critical asset monitoring, ensuring they remain the revenue engine of the entire LBS ecosystem.

Can Legacy GPS Really Fend Off New Contenders? (34.72% Share)

With the rise of Galileo and BeiDou, one might expect the American GPS monopoly to fracture, yet the GPS segment retains a controlling 34.72% market share in the location-based services market. Why? The answer lies in the hardware that defines 2025: the L5 frequency band. While newer constellations are capable, the modernized GPS Block III satellites are beaming the L5 signal with superior power and integrity, making it the industry standard for cutting through the "multipath" interference found in concrete urban jungles. Because reliability is paramount, chipset manufacturers and LBS developers continue to prioritize GPS-specific protocols in their SDKs. When an app developer needs to guarantee a location fix for an on-demand service, they default to the constellation that offers the most robust legacy support and the deepest integration with current hardware, keeping GPS at the top of the technology stack.

Beyond navigation, GPS holds its crown in the location-based services market because it is the heartbeat of the global financial and digital infrastructure. A huge portion of this segment’s market value comes from Stratum 1 timing servers. In 2025, everything from synchronizing 5G network frames to validating timestamps on high-frequency stock trades relies on the precise atomic time provided by GPS. As cyber threats loom larger, enterprise customers are not just buying location; they are buying trust. They pay significantly for encrypted, authenticated GPS signals—leveraging new civilian authentication measures—to secure their operations against spoofing. This entrenched reliance on GPS for time and security keeps it financially ahead of its European and Asian counterparts.

How Did Logistics Finally Eliminate the Blind Spots? (17.6% Share)

Holding a 17.6% share, the Transportation and Logistics segment of the location-based services market has thrived by effectively outlawing uncertainty. In 2025, the industry standard is the Real-Time Transportation Visibility Platform (RTTVP). Shippers have stopped accepting vague status updates; they demand predictive ETAs calculated by algorithms that digest live traffic, weather patterns, and port congestion data. This segment has found a massive profit center in "detention management." By using precise geofencing to record the exact second a truck enters or leaves a yard, these platforms create an immutable audit trail. This eliminates messy billing disputes over driver waiting times (detention fees), providing such a clear Return on Investment that 3PL providers view these subscriptions as non-negotiable.

The technology has also evolved into sensor-fused asset tracking, particularly for the cold chain in the location-based services market. Logistics is no longer just about "where"; it's about "how." LBS solutions now integrate location with condition monitoring—temperature, shock, and humidity—transmitted via efficient Low Power Wide Area Networks (LPWAN). This allows for "intervention logistics." If a pharmaceutical shipment shows a temperature spike while still on the highway, a manager gets an alert instantly and can reroute the driver to a safe facility to save the cargo. By transforming LBS from a simple tracking dot into a proactive risk management tool, this segment has secured its dominance in the global supply chain.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Are Maps Now Built for Machines Instead of People? (21.5% Share)

The Mapping and GIS segment captures 21.5% of the location-based services market, but the product has changed drastically. We are no longer just looking at digital street directories; we are trading in High-Definition (HD) Live Maps designed exclusively for machine vision. The primary customers driving this revenue are automotive OEMs and autonomous system developers who need semantic map layers. These aren't maps for human eyes—they are data streams detailing curb heights, lane curvature, and traffic light topology. The real value innovation here is the "self-healing" map. LBS providers aggregate millions of camera and LiDAR feeds from connected vehicles to update these maps in near real-time, selling this fresh, verified data back to fleets. It is a lucrative, recurring revenue loop where the cars themselves maintain the product they consume.

On the business side, the GIS component of the location-based services market has graduated from static planning tools to dynamic Spatial Business Intelligence. Retailers and urban planners are heavily investing in "Location Intelligence" platforms that overlay real-time mobility patterns with deep psychographic data. For example, Quick Service Restaurants (QSRs) now rely on "white space analysis" to greenlight new locations. Instead of guessing, they use GIS tools to calculate revenue potential based on competitor foot traffic and drive-thru dwell times within specific travel isochrones. This shift from descriptive mapping (showing where things are) to prescriptive analytics (telling businesses where they should be) has turned GIS licenses into essential, high-value corporate assets.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia-Pacific: Super-App Ecosystems and Smart Cities Fueling Half of Global Demand

Commanding a massive 50% market share in location-based services market, Asia-Pacific is the undisputed volume engine of the LBS world. This dominance is not merely demographic but structural; the region’s "Super App" economy—led by WeChat, Grab, and Gojek—has fully integrated location into every digital interaction, from ride-hailing to micro-financing. In China, which alone accounts for over 60% of the regional share, the complete integration of the BeiDou Navigation Satellite System (BDS-3) into consumer electronics now supports decimeter-level accuracy for mass-market phones, bypassing GPS entirely. Meanwhile, India’s market is surging due to the government’s mandate for NavIC (NaVIC) support in all smartphones released post-2025, driving a localized LBS boom in semi-urban logistics. The region’s aggressive rollout of 5G Standalone (SA) networks has also enabled "smart city" projects in ASEAN nations to utilize real-time crowd analytics for traffic management, making APAC the primary testing ground for high-density urban LBS deployment.

North America: Autonomous Fleets and Precision Ad-Tech Driving High-Value Revenue Streams

North America location-based services market retains its position as the highest value-per-user market, driven by the commercial maturation of Level 3 and Level 4 autonomous systems. By 2025, the U.S. market is defined by the monetization of High-Definition (HD) Vector Maps required for autonomous trucking corridors in Texas and California. Unlike APAC’s consumer focus, North American growth is anchored in B2B logistics and precision agriculture, where farmers utilize LBS-guided autonomous tractors to reduce fertilizer costs by 15%. The advertising sector here has evolved into "contextual spatial targeting," where data brokers leverage privacy-compliant SDKs to sell trajectory-based intent data (e.g., predicting a store visit before arrival). This high-margin "predictive location" economy ensures that while North America trails in volume, it leads in average revenue per LBS request.

Europe: Galileo’s Authenticated Precision and Industrial IoT Redefining Regulatory Compliance Standards

Europe’s location-based services market share is carved out by its focus on "sovereign precision" and industrial compliance. The key differentiator in 2025 is the Galileo High Accuracy Service (HAS), which provides free, 20-centimeter accuracy globally. This has become the gold standard for the European automotive insurance market (eCall evolution) and Industry 4.0 asset tracking in the DACH region (Germany, Austria, Switzerland). Unlike other regions, Europe’s growth is legally enforced; the Open Service Navigation Message Authentication (OSNMA) is now a prerequisite for critical infrastructure timing and banking security, effectively locking out non-compliant LBS providers. Consequently, the European market attracts premium stakeholders looking for certified, spoof-proof location data that meets stringent EU AI Act liability standards for autonomous machinery.

Top Players in Location-Based Services Market

- Apple Inc.

- AT&T Inc.

- Bharti Airtel Limited

- Cisco Systems, Inc.

- ESRI

- Google LLC

- HERE Technologies

- IBM Cooperation

- Microsoft Cooperation

- Oracle Cooperation

- Qualcomm Technologies, Inc.

- TomTom N.V.

- Zebra Technologies

- Other Prominent Players

Market Segmental Overview

By Components

- Solutions

- Location Intelligence Solutions

- Location-powered Mobile Applications

- Location-based Messaging

- Services

- Professional

- Managed

By Location Type

- Indoor

- Outdoor

By Technology

- Global Positioning System (GPS)

- Global Navigation Satellite System (GNSS)

- Wi-Fi

- Cellular ID

- Bluetooth beacons

- Others

By Application

- Inventory Monitoring

- Mapping & GIS

- Asset Tracking

- Proximity Marketing

- Social Networking

- Fleet Management

- Navigation

- Smart Parking

- Route Planning

- Business Intelligence & Analytics

By End User

- BFSI

- Manufacturing

- Retail

- Healthcare & Life Science

- IT & Telecom

- Hospitality

- Transportation & Logistics

- Government

- Media & Entertainment

- Aerospace & Défense

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The U.K.

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of Middle East & Africa

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 77.69 Bn |

| Expected Revenue in 2033 | US$ 547.92 Bn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 24.2% |

| Segments covered | By Components, By Location Type, By Technology, By Application, By End User, By Region |

| Key Companies | Apple Inc., AT&T Inc., Bharti Airtel Limited, Cisco Systems, Inc., ESRI, Google LLC, HERE Technologies, IBM Cooperation, Microsoft Cooperation, Oracle Cooperation, Qualcomm Technologies, Inc., TomTom N.V., Zebra Technologies, Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |